High-Risk Gateways

High-Risk Payment Gateways: Building Stable Processing for Industries Banks Don't Love

Why "high-risk" is mostly a label about infrastructure mismatch rather than business quality, and how the right gateway turns it into a competitive position rather than a constant operational headache.

The term high-risk merchant gets thrown around as if it were a verdict on the business itself. In practice, it usually says more about the infrastructure that's evaluating the business than about the business's actual integrity. Plenty of well-run, profitable, fully compliant companies sit inside the "high-risk" bucket simply because they operate in industries, gaming, crypto, travel, subscriptions, forex, CBD, adult, financial services, that don't match the assumptions traditional payment infrastructure was built around.

Standard gateways were designed for predictable, low-dispute, single-jurisdiction commerce. The moment a business deals in high transaction volumes, cross-border flows, recurring billing, or a regulated vertical with above-average chargeback exposure, the standard model starts squeezing rather than supporting them. Acquirers refuse to onboard. Account freezes appear without warning. Approval rates drop quietly. Settlement timelines stretch. The merchant ends up running their business on infrastructure that was never built for it.

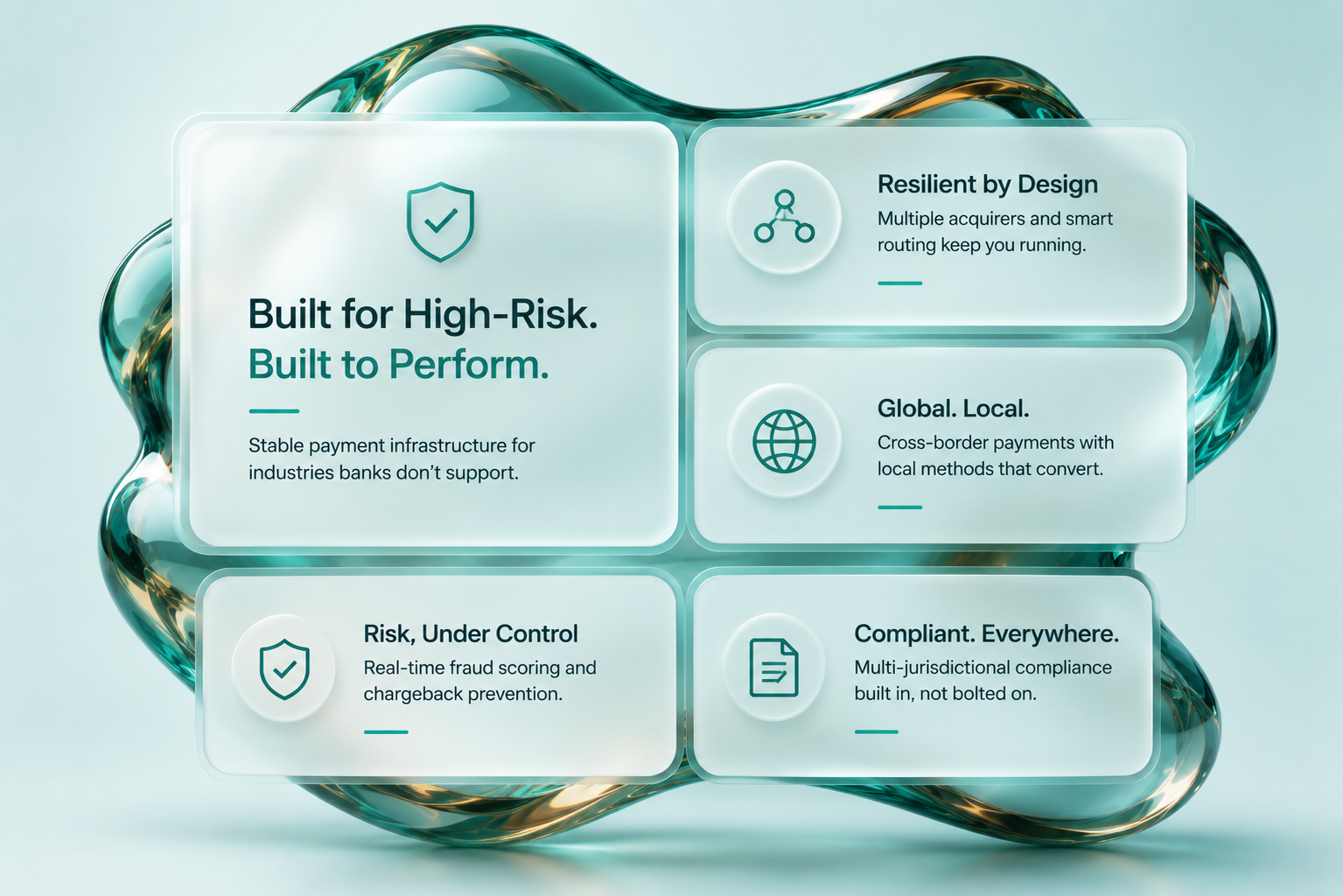

A high-risk payment gateway isn't a workaround for businesses with problems. It's purpose-built infrastructure for industries that the conventional stack handles badly. Used well, it stops being a defensive tool and starts being a structural advantage, the layer that lets a complex, high-volume, cross-border business actually scale.

What a High-Risk Payment Gateway Actually Is

At its core, a high-risk gateway is a payment infrastructure designed for merchants whose transaction profile sits outside what mainstream acquirers will comfortably underwrite. Where a standard gateway depends on a single acquirer, a small set of fraud filters, and generic onboarding, a high-risk gateway is built to handle the things that make the standard model brittle: chargeback volatility, regulatory complexity, cross-border flows, and the uneven appetite of acquiring banks for specific verticals.

The way it accomplishes that, technically:

- Multiple acquiring relationships rather than dependency on a single bank

- Real-time, behaviour-driven risk scoring rather than static rule sets

- Dispute and chargeback management tooling built into the gateway, not bolted on

- Global card and APM coverage so a merchant isn't trapped in a single payment culture

- Compliance frameworks that handle multiple jurisdictions concurrently

The combination is what allows a high-risk merchant to keep accepting payments cleanly in markets that most processors would either refuse to serve or quietly throttle.

Who Actually Operates Under "High-Risk" Conditions

The label spans a wider range of industries than people typically realise. A non-exhaustive list:

- Online gaming and sports betting, where regulatory complexity and dispute volumes are both high

- Crypto exchanges and digital asset platforms, where banking partners are scarce and conditions tightening

- Travel and airline platforms, where forward sales, refund spikes, and operator disputes drive elevated chargeback rates

- Subscription and continuity-billing models, particularly anything resembling free-trial-to-paid

- Forex and trading platforms, with their characteristic dispute and AML profile

- Adult entertainment and CBD verticals, where the issue is acquirer appetite more than transaction risk per se

- Financial services, including lending, neobanks, and remittance-style flows

What unites them isn't bad behaviour. It's the combination of high volume, cross-border activity, recurring revenue dynamics, and exposure to disputes or regulatory scrutiny that standard gateways aren't tuned to handle.

For these merchants, an unsuitable gateway isn't an inconvenience. It's an existential vulnerability. A frozen account, a single acquirer pulling out, or a chargeback ratio drifting out of compliance can cut off processing overnight.

Where a High-Risk Gateway Differs From a Standard One

The differences are more than incremental. Side by side:

CapabilityStandard GatewayHigh-Risk Payment GatewayFraud protectionStatic filters and basic rulesAI-driven scoring, behavioural analysis, layered controlsAcquiring networkSingle acquirer dependencyMulti-acquirer redundancy with smart routingChargeback handlingReactive, limited toolingProactive prevention, alerts, dispute response automationCompliance scopeStandard PCI, single jurisdictionMulti-jurisdictional, vertical-specific frameworksOnboardingFast, generic underwritingDeeper underwriting matched to vertical realitiesRouting logicMinimal, single path per transactionDynamic routing across acquirers based on approval likelihoodSettlement flexibilityLimited currency and payout optionsMulti-currency, varied payout structures

The structural difference is that a high-risk gateway treats payment processing as a portfolio problem, multiple acquirers, multiple rails, multiple risk signals working together, rather than a single-thread pipeline. That portfolio model is what gives it resilience.

What High-Risk Payment Processors Actually Do

Behind every high-risk gateway sits a network of processors, the entities that physically move funds between customers, banks, and merchants. The gateway is the orchestration layer; the processors are the rails.

What separates a high-risk processor from a standard one isn't a single technical feature; it's the operational posture:

- Vertical specialisation. They understand the chargeback patterns, regulatory rhythms, and seasonal volatility of specific industries.

- Higher approval ratios on difficult verticals. Their underwriting and rule sets are tuned to convert legitimate transactions in environments where mainstream acquirers would over-decline.

- Custom routing logic. Each transaction can be sent to the processor most likely to approve it given the merchant, the customer, the BIN, and the vertical.

- Risk-tiered pricing. Costs are transparently aligned with risk exposure rather than averaged across the merchant base.

- Multi-currency and multi-region support. Especially important for genuinely cross-border merchants.

A good gateway pulls these processors into a single, coherent flow, so the merchant gets the resilience of a multi-processor setup with the operational simplicity of a single integration.

What to Look For When Choosing One

The market for high-risk gateways is not small, and not all providers offer the same depth. Areas worth scrutinising carefully:

Multi-acquirer connectivity. The single most important capability. If your gateway runs on one acquiring relationship, your business runs on one acquiring relationship, and the day that bank decides it's done with your vertical, you have a serious problem.

Smart routing. Static "primary plus fallback" logic is no longer enough. The gateway should route each transaction dynamically based on approval likelihood, cost, time of day, and current acquirer health.

Built-in compliance tooling. PSD2/SCA, PCI DSS, AML screening, and the local frameworks that apply in each market the merchant operates in. Compliance handled by the gateway is compliance you don't have to engineer separately.

Chargeback prevention and management. Pre-dispute alerts, network-tokenisation support, and dispute response automation. For high-risk merchants, chargeback ratio is the metric that determines whether processing stays online. Getting this layer right is non-negotiable.

Analytics with depth. Approval rates broken out by acquirer, BIN, country, and method. Chargeback trends. Fraud signals. Decline reason distributions. Aggregated dashboards that hide where the actual problems live aren't useful at scale.

Flexible settlement. Multi-currency, varied payout schedules, and clean reconciliation across the entire flow.

Operational support. When something does go wrong, and in high-risk processing, something always does eventually, there's a meaningful difference between a vendor that surfaces the issue with context and one that hands the merchant a generic decline code.

What Makes High-Risk Processing Genuinely Hard

There's no point pretending the operating realities are easy. Even with the right gateway, high-risk merchants navigate a tougher environment than mainstream ones:

- Higher processing fees, reflecting the genuine risk exposure being absorbed by acquirers and processors

- Longer underwriting cycles, as providers do real diligence rather than rubber-stamp onboarding

- Stricter documentation requirements, both at onboarding and on an ongoing basis

- Sustained scrutiny from card networks, with chargeback ratio thresholds being enforced consistently

- Regulatory volatility, particularly in crypto, gambling, and forex, where rules can shift quickly

These conditions don't disappear with the right gateway. What changes is how manageable they become. A vertically specialised gateway, paired with multiple processors, real-time monitoring, and diversified banking, turns these from existential threats into operational variables that can be tuned and contained.

Why the Strongest Operators Treat This as a Strategic Layer

The merchants who outperform in high-risk verticals tend to share an attitude: they treat their payment infrastructure as a competitive weapon, not a back-office function.

What that looks like in practice:

- They don't accept single-acquirer dependency under any circumstances

- They route dynamically rather than statically

- They monitor approval rates at granular level, by market, BIN, method, and acquirer, not as a single global average

- They feed real-time risk signals into routing decisions, so high-risk transactions can take stricter routes while low-risk ones move freely

- They diversify banking relationships proactively, before they need to

- They treat chargeback management as continuous work, not crisis response

The result is something most high-risk merchants never achieve: stable processing in markets that most providers consider too volatile to serve. That stability translates directly into higher acceptance rates, lower churn, more predictable cash flow, and better unit economics, exactly the things mainstream merchants take for granted.

Where This Is Heading

The trajectory of high-risk processing is clear enough to plan around. Three trends in particular are reshaping how the next generation of gateways will operate:

Machine learning at every layer. Risk scoring, routing, dispute prediction, and approval optimisation all benefit from models that learn from each transaction. Static rule engines are increasingly inadequate against AI-augmented fraud.

Real-time compliance. Regulators across multiple jurisdictions are moving toward live transaction monitoring rather than after-the-fact reporting. Italy's SIC system has demonstrated what this looks like in practice; similar regimes are spreading.

Cross-network orchestration. The value of consolidating multiple processors, multiple rails, and multiple methods under a single intelligent layer keeps growing. Fragmented setups don't scale.

The merchants who get ahead of these shifts won't experience them as disruptions. They'll experience them as upgrades.

The Bottom Line

Being a high-risk merchant doesn't mean operating with worse tools. It means operating with different tools, ones designed for the realities of the industries that mainstream payment infrastructure simply wasn't built to handle.

Done right, a high-risk payment gateway turns processing from a recurring source of stress into a stable, predictable layer the rest of the business can confidently grow on top of. That stability is what separates merchants who survive in volatile verticals from those who quietly thrive in them.

At Paylinq, we build payment infrastructure for merchants whose verticals don't fit the mainstream model, gaming, crypto, travel, subscriptions, forex, and other industries where standard gateways start to creak. Through a single platform, our clients access multi-acquirer routing, vertically tuned risk controls, integrated compliance, and dedicated operational support, designed to keep processing stable and approval rates high in environments most providers find difficult. If you'd like to map out what stronger high-risk infrastructure would look like for your business, get in touch with our team.

This article is provided for informational and educational purposes only and does not constitute financial, legal, tax, regulatory, or compliance advice. Specific operational, payment, and risk decisions, particularly in high-risk verticals, should be made in consultation with qualified professionals familiar with your jurisdiction and business model. References to specific industries, regulations, providers, or scenarios are illustrative only and do not imply endorsement or guarantee. The authors and publisher accept no liability for actions taken based on this content. Information may become outdated as payment infrastructure, regulations, and market conditions evolve.

Simple. Fast. Reliable.

At Paylinq, we deliver a seamless experience with full transparency and effortless operations, so payments just work.

Social Handle