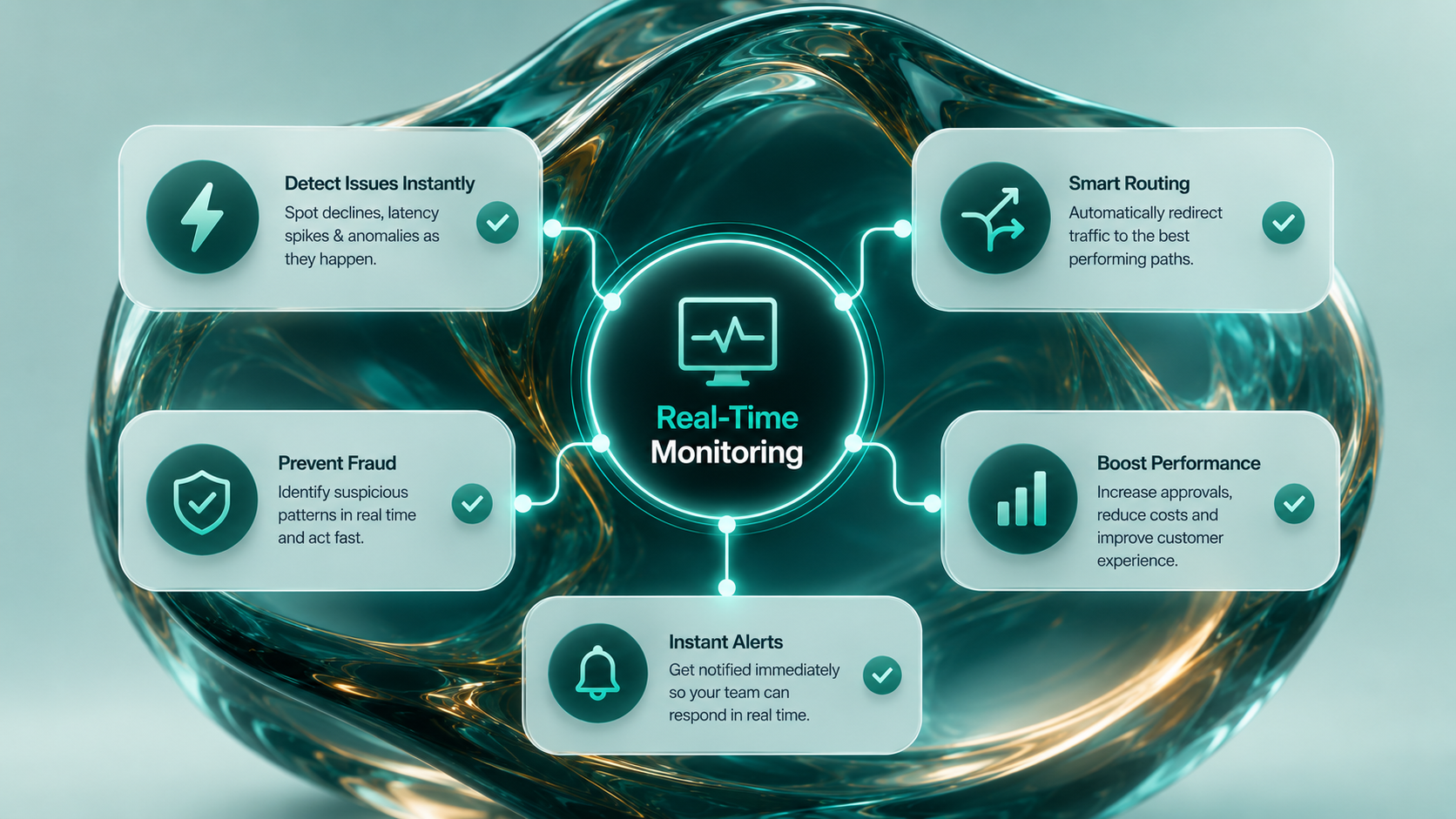

Live Monitoring

Real-Time Transaction Monitoring: Closing the Gap Between What Just Happened and What You Can Do About It

Why batch reporting belongs to a slower era of commerce, and how live monitoring inside a payment orchestration layer turns every transaction into a chance to optimise - not a number to look at tomorrow.

There's a quiet problem at the centre of how most payment operations are still run: the data telling you something is wrong almost always arrives later than the moment you needed it.

A provider's approval rate slips during a peak hour. A specific BIN range starts declining at unusual rates. A processor's latency creeps up just enough to drag completion rates down without throwing a clear error. By the time the daily report lands the next morning, the affected window has already closed. Customers who would have completed checkout didn't. Transactions that could have been recovered weren't. The opportunity to react existed, but only for the team that could see what was happening as it was happening.

This is the gap real-time transaction monitoring is built to close. Inside a payment orchestration layer, live monitoring stops being a dashboard exercise and becomes the feedback loop that drives the entire stack: routing, retries, risk decisions, alerts, optimisation. The shorter that feedback loop, the better every other layer performs.

For merchants serious about approval rates, fraud prevention, and operational resilience, this is no longer an optional analytics upgrade. It's part of the architecture.

What Real-Time Transaction Monitoring Actually Means

The phrase covers a specific capability: tracking and analysing every transaction the instant it happens, rather than waiting for batch reports to summarise what already occurred.

Every authorisation, decline, retry, refund, and authentication step generates data. In a real-time monitoring setup, that data flows into a live view immediately - not in hourly aggregates, not in end-of-day reports, but as the events unfold. The result is a continuously refreshed picture of what's happening across the entire payment stack.

The practical effect is that several things become possible that simply aren't with batch reporting:

- Performance issues can be spotted as they emerge, before they cause meaningful damage

- Suspicious or unusual transaction patterns surface quickly, while there's still time to intervene

- Failed or under-performing transactions can be rerouted automatically through alternative paths

- Approval rates and costs are visible to the second, rather than as historical artefacts

- Decisions are made on what's true now, not what was true earlier today

The shift sounds incremental on paper. In practice it changes what a payment operation can actually do.

Why Batch Reporting Was Always Going to Hit a Wall

Batch reporting served a particular era of commerce - one with predictable hours, slower transaction volumes, smaller cross-border footprints, and fewer providers in the mix. It was good enough because the underlying systems didn't move fast enough to require anything more.

That era is over.

Modern payment stacks are stitched together from many providers - gateways, acquirers, fraud vendors, APMs, FX engines, risk tools - each with their own performance curves and failure modes. Volumes spike unpredictably with promotions, sports calendars, and viral moments. Providers can degrade or recover within minutes. Fraud patterns shift across continents while the affected merchant is still asleep.

In that environment, relying on yesterday's report to make today's decisions is a recipe for being permanently a step behind. The damage doesn't accumulate visibly; it accumulates as quiet drift - slightly lower approval rates, slightly higher fraud losses, slightly worse customer experiences - that's hard to attribute to any single cause and easy to absorb until it stops being absorbable.

Batch reporting still has its place for reconciliation, accounting, and end-of-period analysis. But running an operation on it is a structural disadvantage.

Real-Time Data as the Engine for Dynamic Routing

The first place live monitoring earns its keep is in routing. Smart routing only works as well as the information it's making decisions on. If routing logic is operating on yesterday's averages, it's optimising for conditions that no longer exist.

When monitoring is live, routing becomes a meaningfully different layer:

- Provider degradation gets routed around in real time. A processor whose approval rate has just dropped or whose latency is climbing receives less traffic until it recovers.

- Region- and BIN-specific shifts trigger immediate adjustments. If approval rates on UK-issued cards through a specific acquirer dip mid-afternoon, traffic redistributes within minutes.

- Retry logic gets smarter. A failed transaction is retried against an alternative path that, in the current moment, is performing well - not against whatever a static rule says is "the backup."

- High-risk transactions can take stricter routes selectively. Without forcing every transaction through the same risk tier.

The compound effect is consistent: more transactions approved, fewer customers leaving with abandoned carts, and a payment system that responds to live conditions instead of yesterday's snapshot.

The Operational Visibility That Makes Teams Faster

Beyond routing, live monitoring fundamentally changes what payment, finance, product, and risk teams can do day-to-day. The dashboards aren't decoration - they're operational tools.

What a properly built monitoring layer surfaces:

- Performance by provider, region, payment method, BIN, and card type - not just global averages that hide where problems live

- Latency and success-rate trends in time horizons that allow intervention rather than postmortem

- Automated alerts on meaningful shifts in approval rates, decline reasons, fraud signals, or processor health

- Decline-reason distributions that reveal whether issues are technical, risk-related, or customer-side

- Authorisation-to-settlement tracking that catches funds-flow problems before they hit reconciliation

- Single source of truth for teams that historically each ran on their own delayed extracts

The cultural effect is at least as important as the technical one. When everyone is working from the same live picture, debates about what's happening shrink and time spent on what to do about it grows. Problems are caught and contained before they reach customer-facing impact - which is, ultimately, the point.

What This Adds Up To, Concretely

Stripped of buzzwords, the practical advantages of real-time monitoring inside an orchestrated payment stack land in a few specific places:

Higher approval rates. Transactions that would have failed under static routing get rerouted while there's still a chance of approval. Aggregated across volume, this is a measurable lift.

Lower fraud losses. Suspicious patterns get caught and stopped at the point of authorisation, not flagged in a report after the funds have moved.

Lower processing costs. Automated routing across providers based on live performance and cost data prevents the slow accumulation of fees that static setups absorb without noticing.

Stronger customer trust. Customers don't see the routing logic, but they feel the result: fewer payment failures, faster checkouts, more consistent experiences across markets and devices.

Better strategic decisions. Live, granular data is the foundation for confident moves - entering a new market, switching acquirers, adjusting risk thresholds - that would otherwise rely on guesswork or delayed signals.

Each of these has a dollar value attached to it that compounds with volume.

When Real-Time Monitoring Becomes Non-Negotiable

For very small merchants with a single provider in a single market, batch reporting may still be enough to operate on. The threshold at which that stops being true tends to coincide with one or more of these conditions:

- Multiple providers in the stack. The more moving parts, the higher the value of seeing them simultaneously.

- Cross-border volume. Performance varies by region and changes throughout the day; yesterday's averages mask today's reality.

- Subscription or recurring billing. Failed renewals cost more than failed one-off purchases because they break long-term revenue, making timing of intervention especially valuable.

- High-risk verticals. Fraud and approval-rate volatility are higher; the cost of missing a shift is larger.

- Peak-driven business models. Sports calendars, retail seasonality, campaign-driven traffic - anything where short windows carry disproportionate revenue weight.

Hit any combination of these and operating on delayed data is no longer a small inefficiency; it's a constraint on growth.

Where This Is Going

The trajectory is clear. Real-time visibility is becoming the assumed baseline rather than the premium feature, for two converging reasons.

The first is regulatory. Several European markets are moving toward live transaction reporting obligations - Italy's SIC system being the most cited example, with similar regimes expanding. Operating without real-time monitoring will increasingly be operating outside compliance, not just outside best practice.

The second is competitive. Merchants who can see and act in real time consistently outperform peers who can't, on every metric that actually matters: approval rates, fraud control, cost efficiency, customer experience. As the gap widens, the pressure to close it intensifies.

The merchants who treat real-time monitoring as part of their operational architecture, rather than as a dashboard sitting alongside it, are the ones who will define the next stage of payment performance.

The Bottom Line

Payments don't fail at a single point. They fail incrementally - a slightly slower processor here, a slightly worse approval rate there, a fraud pattern building over an afternoon - and the merchants who absorb those losses without ever seeing them clearly are the ones running on yesterday's data.

Real-time transaction monitoring, properly integrated into a payment orchestration layer, closes the loop between what's happening and what you can do about it. It's the difference between watching the past and shaping the present.

In an environment where margins on every transaction are tight and customer expectations on every checkout are tighter, that loop is no longer optional architecture. It's where competitive payment performance actually lives.

At Paylinq, we build payment infrastructure where real-time monitoring sits at the centre rather than at the edge. Through a single orchestration layer, our clients see performance across providers, markets, BINs, and methods as it unfolds - and route, retry, and intervene based on what's actually happening, not what happened yesterday. If you'd like to see how live monitoring would look applied to your stack, get in touch with our team.

This article is provided for informational and educational purposes only and does not constitute financial, legal, tax, regulatory, or compliance advice. Specific operational, payment, and monitoring decisions should be made in consultation with qualified professionals familiar with your jurisdiction and business model. References to specific regulations, providers, or scenarios are illustrative only and do not imply endorsement or guarantee. The authors and publisher accept no liability for actions taken based on this content. Information may become outdated as payment infrastructure, regulations, and market conditions evolve.

Simple. Fast. Reliable.

At Paylinq, we deliver a seamless experience with full transparency and effortless operations, so payments just work.

Social Handle